MITIGATING INCREASES IN THE PRICE OF ELECTRICITY CAUSED BY DATA CENTER DEMAND: PART ONE

Identifying When and How Data Center Demand Can Cause Electricity Prices to Increase

I know that, notwithstanding my hypothetical monthly publication schedule, it’s been seven weeks since my last post. Sorry about being so late. My life has been very hectic, with lots of travel and other activities, including work on my book. And this has been a hard post to write; a lot of words were left on the cutting floor of my editing room. I will post my next article in a month or less, I (hypothetically) guarantee.

In the meantime, a number of new people have subscribed or followed Explaining the Grid since my last post. Welcome to all of you. I try to write largely jargon and acronym free posts that are understandable to reasonably intelligent people, which by definition you all are. since you are reading my Substack. This post, like all others, is based on my best analysis and not on politics or name-calling. Let me know if you think I got something wrong and, if I agree with you, I will make a correction.

The inspiration for today’s post comes from J.P. Morgan’s 16th Annual Eye on the Market Energy Paper, written by Michael Cembalest, entitled Fighting Words. (Check it out, you can find it here. Fighting Words) One of the topics in J.P. Morgan’s paper is entitled “Data centers: the pitchforks are gathering regarding their impact on US power prices.” As the name implies, the discussion describes the growing concern that recent increases in retail electricity prices in many states have been caused by data centers’ high and still growing demand for electricity. That topic inspired me to write a post about different proposals to address the effect of data center demand on electricity prices.

As I started to write my post, however, I realized that before I can discuss price mitigation proposals, I first have to explain how, if at all, data centers are causing electricity prices to increase. Anyone who reads the news knows that data centers are not very popular right now, in part because a large segment of the population is skeptical about AI. One easy way to attack AI is to claim that data centers are responsible for electric price increases. In writing my post I quickly learned that any discussion of the effects of data center demand on electricity prices is complicated. I decided that the best course is to write a two-part article, the first (this one) addressing the question of how data centers affect electricity prices, and the second (the next one) on proposals to mitigate electricity price increases caused by data centers.[1]

Let me start by noting that, to date, data centers’ demand for electricity does not explain most of the currently high electricity prices. Those prices have resulted primarily from other factors, including: (1) 13 straight years of record breaking investment in transmission and distribution facilities—more than $1.3 trillion over the last 10 years—primarily to harden the grid against wildfires, floods, and hurricanes and to interconnect with renewable generation facilities; (2) the inclusion in rates the cost of subsidies for renewable generation facilities as well as the costs of social programs completely unrelated to the grid; (3) the use of large amounts of expensive oil-fired generation in the winter as a consequence of inadequate natural gas pipeline capacity; and (4) higher prices for natural gas following Russia’s invasion of Ukraine. I am sure that data centers have received at least some of the blame for the price effects of these unrelated factors.

The effect of data center demand on the price of electricity was discussed in a recent October 10, 2025 joint study by the Lawrence Berkeley National Laboratory and the Brattle Group (Factors Influencing Recent Trends in Retail Electricity Prices in the United States: What do we know? Where are the gaps?). This study concluded that, contrary to the claim increased demand from data centers is causing retail electric price increases, the states with the highest demand growth over the previous five years actually saw a decline in their electric prices. By contrast, states whose demand declined often saw increases in the price of electricity. The study concluded that the greater use of the grid’s assets resulting from meeting higher demand allowed the costs of those assets to be spread over a greater amount of electricity sales, thereby lowering the cost per unit of electricity sold. It’s like inviting a family to share your beach house for a week. Splitting the cost between the two families significantly reduces the cost each family has to pay.

But at some point, your beach house won’t hold any more people, and another house will have to be rented if more families want to come. Similarly, the cost of producing and transmitting electricity will go up when the grid needs to add new infrastructure to serve data centers’ increased demand. And significant new infrastructure is starting to be required. The potential resulting cost increases can be separated into three categories: (1) the cost of new generation facilities; (2) the cost of new transmission and distribution facilities; and (3) the wholesale price of electricity. This post will discuss each of these three categories. I also will discuss a fourth factor, perhaps the most important factor of all: how these costs incurred by utilities selling electricity at retail to consumers are reflected in the price they charge for electricity.

Cost of Generation Capacity

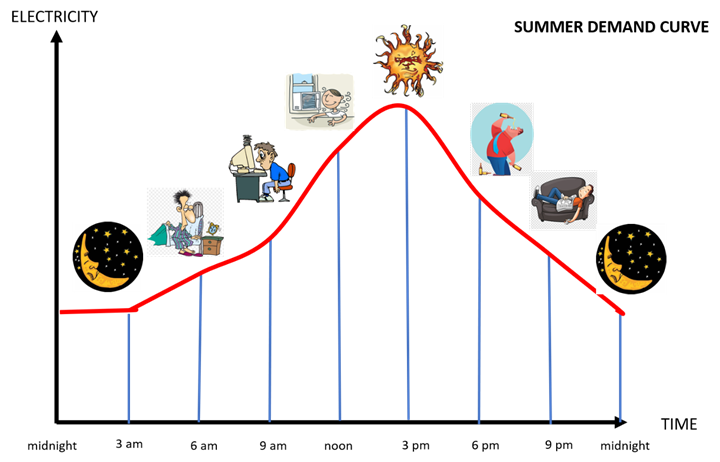

It is intuitively obvious that increased data center demand for electricity will, at some point, require new generation capacity to supply that increased demand. I think it is helpful, however, to explain exactly how this happens. That knowledge will be especially important in my next post discussing ways to mitigate the price effects of increased demand. To do this, I am going to dust off one of my not very good old graphics—THE CURVE—which I haven’t used in a while.

To start the discussion, I first am going to present THE CURVE in its most basic form.

This version of THE CURVE illustrates how the amount of demand for electricity on the grid changes during the day and night in the summer. The curved red line shows the amount of demand at different times of the day. As you can see, demand is low at night when most people are asleep. But it is not zero, because some people are up, your refrigerator and AC are running, streetlights are on, etc. Demand increases as people wake up, go to work or school, and increases further as the temperature gets hotter. Demand peaks in the afternoon when the temperature is at its highest, and then declines as the temperature drops, people go home, have dinner and eventually go to bed. (The shape of the demand curve varies among different electric systems and changes in the winter, but this does not affect the point I am making here)

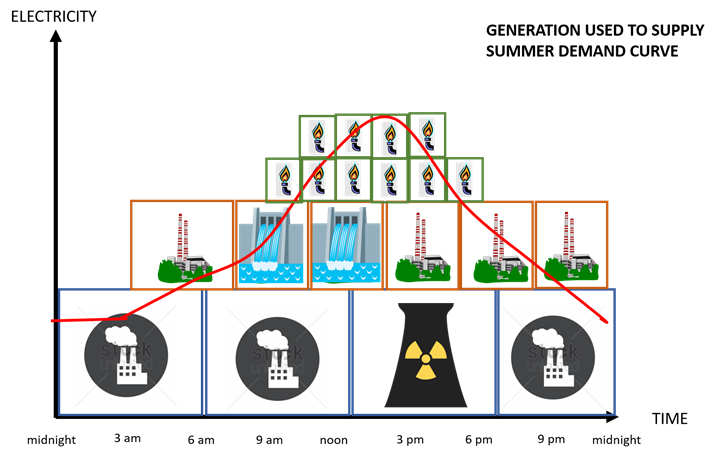

The next version of THE CURVE shows why the shape of the demand curve has important implications for the grid.

As you can see, I have inserted into THE CURVE the different types of generation needed to supply demand throughout the day. The bottom row consists of large generators, known as “baseload” generators. that operate all day and night. Baseload generators are the only generators needed when demand is low at night, but as demand increases throughout the day additional generators also need to be turned on. The second row consists of somewhat smaller “intermediate” generators that run for much of the day but typically not that much at night. The third row includes even smaller generators and the fourth row the smallest generators, known as “peakers.” The peakers are used in the relatively few hours in the middle of the day when the electric system’s demand is at its highest; known as the peak (I could have put some wind and solar generators in the graphic but that adds a layer of complexity not needed for the point I am making here).

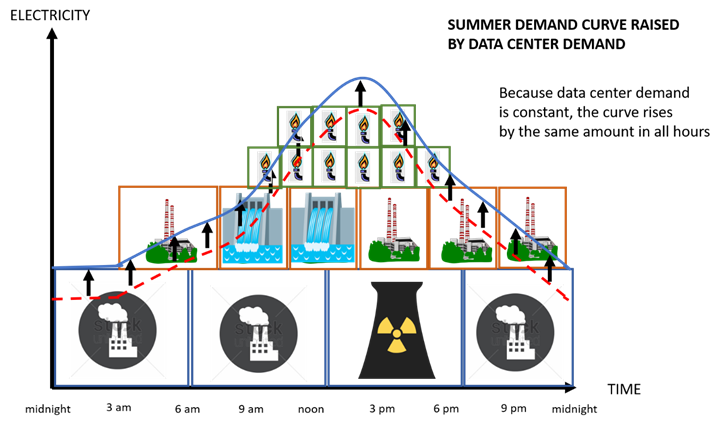

The final version of THE CURVE shows the potential problem raised by increased data center demand.

As you can see, data center demand is relatively constant all day, so it increases total system demand by about the same amount each hour of the day. For most of the day, there is more than enough generation capacity to serve all demand even when the data center demand is included. It is only when, as shown in the graphic, data center demand causes the peak system demand to exceed an electric system’s entire complement of generation that there is a problem. And this problem lasts for only a short time, at most a few hours, during the time of peak demand.

Typically, data center demand will not exceed an electric system’s total generation capacity, even during peak demand hours. All electric systems are required to acquire more generation capacity than they project will be needed during their highest peak demand hours. This difference between an electric system’s total generation capacity and its expected peak demand is known as its capacity reserve margin.

Capacity reserve margins shrink as demand increases. To keep the margins at appropriate levels, new generation capacity must be added to offset the increase in demand. And sufficient new generation capacity has not been constructed. Studies performed by the North American Electric Reliability Corporation—the entity designated by Congress to ensure the grid’s reliability—and by the Department of Energy have identified potential generation capacity shortages in the near future. To date, the forecasted potential blackouts would occur only in the event of extraordinary circumstances, such as very high temperatures and greater than normal generator outages in the summer, or very cold weather that forces generators offline in the winter. As of yet, no one has forecast blackouts under typical operating conditions.

In saying this, I am not trying to make light of the problem. Several regions in the US have suffered from major heat waves and/or severe winter storms in the past few years. It appears likely that we will continue to suffer from extreme summer heat and winter cold in the future. Without sufficient new generation capacity additions, it is inevitable that large regions of the country will suffer from persistent rolling blackouts in the near future.

This need for new generation capacity has already had an effect on generation capacity prices. For example, the price for capacity currently being charged by the PJM Regional Transmission Organization (RTO), established in an auction conducted in 2024, reflects the need for new generation capacity to serve rapidly increasing data center demand for electricity. That price, $270 per megawatt/day,[2] is about 10 times higher than the capacity price for the previous year, and about $100 higher than the highest price prior to the current year. The PJM capacity prices in PJM’s following two auctions, which will take effect in June of 2026 and June of 2027 respectively, are about $60 higher than the current capacity prices.[3] Despite this high price, the most recent PJM capacity auction failed to acquire the amount of generation capacity PJM determined was necessary to ensure the reliability of its system.[4] Similarly, capacity prices have gone up in the last few years’ auctions in the three other RTOs that conduct capacity auctions (ISO-New England, New York ISO, and the Midcontinent ISO).

It is important to note that the capacity prices established in the RTO capacity markets are paid to all generators receiving capacity contracts. And all utilities located in an RTO that sell electricity to retail customers must acquire capacity from the RTO at the capacity auction market price. Consequently, high capacity prices resulting from increased data center demand for electricity increase the costs incurred to provide electric service to all retail customers in these RTOs. Outside of the RTOs, electric utilities also need to construct or purchase new capacity to maintain their capacity reserve margins, the cost of which also must be recovered in their prices for electricity.

Cost of New Transmission and Distribution Facilities

In addition to requiring new generation capacity, upgrades to transmission and distribution facilities may be required to deliver electricity to data centers. These upgrades can be expensive, with costs in the hundreds of millions of dollars. The need to construct these expensive upgrades to serve data centers is frequently cited by opponents who argue that data centers have caused increases in electricity prices.

As I noted near the beginning of this post, there has been record investment in the grid’s transmission and distribution systems for 13 years in a row, and this investment represents a significant factor in electricity price increases. This investment, however, was not driven by increased data center demand but instead has primarily been directed towards hardening the grid against natural disasters and interconnecting the grid with wind and solar generation facilities in remote locations. The increase in demand associated with data centers has been too recent to have had much of an impact on transmission and distribution upgrade costs to date.

Data center demand certainly is driving the need for future transmission and distribution upgrades. However, any future upgrade cost increases resulting from data center demand for electricity likely will be largely offset by the revenues from data centers’ increased use of the existing transmission and distribution system. As we saw on the various versions of THE CURVE graphic, the grid operates at levels well below its maximum capacity for most of the day, especially in the night hours. This means there is more than enough transmission and distribution capacity in most, if not all, hours of the day to deliver the increased amount of electricity needed by data centers on a 24/7 basis. As the Lawrence Berkeley National Laboratory/Brattle Group joint study showed, higher demand reduces the per unit price of electricity needed to cover the costs of facilities. When upgrade costs are considered in conjunction with the revenues resulting from increased transmission and distribution revenues, the effect of increased data center demand on transmission and distribution system costs should not be significant.

Wholesale Cost of Electricity

A not very well known effect of increased data center demand for electricity is that the higher demand should increase the wholesale cost of electricity. I will return to my frequently-used graphic, THE STACK, to explain why this is so.[5] This discussion likely will be repetitive for those of you who have met THE STACK before, but hopefully it will be useful to my new subscribers.

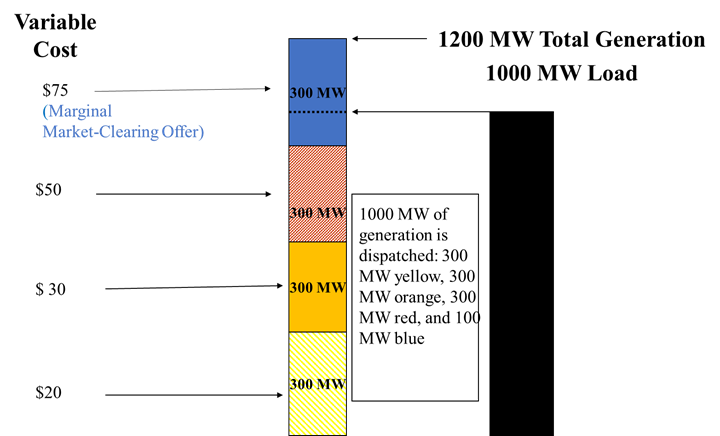

If you have already read any of my previous posts where THE STACK made an appearance, then you know how this works. To recap, all offers to sell electricity in an RTO wholesale market are stacked, from lowest cost offer to highest cost offer. The RTO then determines how much customer demand exists, and then compares the total amount of customer demand with THE STACK. The highest priced offer needed to serve the last megawatt of customer demand—known as the marginal offer or the market-clearing offer—and all lower priced offers, receive awards to sell electricity. And every winning generator is paid the market-clearing price even if it offered to sell at a lower price. If you want to know why everyone gets that price, read Explaining the Grid Part Four—RTO Energy Markets.

If you look at THE STACK, you can probably figure out quickly how an increase in demand can increase the price of electricity. If an increase in demand results from data centers’ need for large amounts of electricity, the total demand can easily move up the stack to the next highest cost offer to sell electricity, as shown by the following version of THE STACK:

Demand has increased by 150 MW, from 850 MW to 1000 MW. This increase in demand has moved the price of the marginal market-clearing price from $50 to $75. And that increase in the marginal market-clearing price means the entire 1,000 MW of electricity is sold at a price of $75/MW, a $25/MW increase in price caused by increased data center demand for electricity.

The actual setting of prices in RTO markets is much more complicated because there are hundreds, if not thousands, of offers submitted into those markets, and in the energy markets prices are calculated as often as every five minutes. And because there are so many more offers being submitted, the difference in prices between offers is usually much less than shown in my STACK graphic. But the general principle is the same. An increase in demand for electricity can cause an increase in the wholesale price of electricity, at least in the short run.

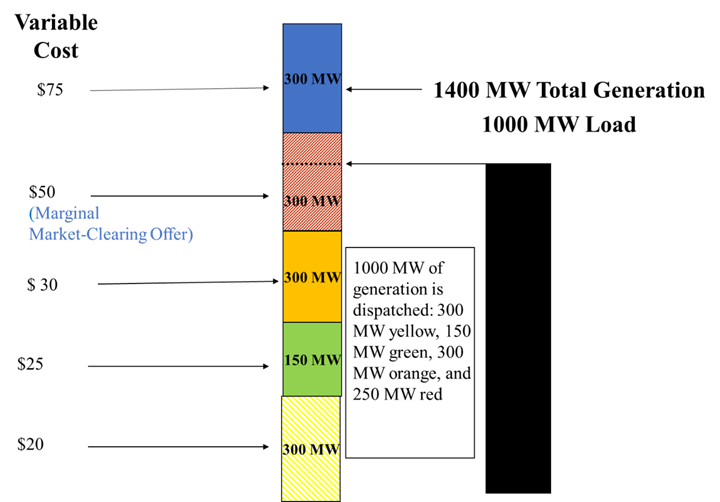

This does not necessarily mean that the increased demand for electricity caused by data centers will lead to higher prices in the RTO wholesale markets in the longer term. As the demand for electricity in an RTO increases, so will the amount of generation capacity (hopefully). And if the new generation capacity is able to offer its electricity into the market at a relatively low price, that lower price offer could offset the price effects of the increase in demand, or even result in a decrease in the RTO market price. This is illustrated by the third and last of my STACK graphics. In this graphic, the 150 MW increase in demand is accompanied by an offer from a newly constructed low cost generation facility (shown in green on THE STACK) at a price of $25. This new offer moves the higher priced offers up in the stack so that the marginal cost offer once again comes from the facility offering to sell at $50. Because the 150 MW increase in demand was offset by the new low cost generation facility, the increase in demand had no effect on the market-clearing offer price, returning the market price to $50, where it was before data centers caused the demand for electricity to increase.

It is impossible to know today whether and when newly constructed generation facilities might offset increased data center demand. But for the near future at least, it appears likely that demand will increase faster than supply. If that happens, the likely result will be an increase in the wholesale cost of electricity.

Recovery of Increased Costs in the Retail Price of Electricity

Up to now, we have discussed how increased data center demand for electricity has affected the costs incurred by utilities that sell electricity at retail to consumers. But that is not the end of the story. Utilities develop rates governing the price of the electricity they sell, based on the costs they incur. Regulators, typically a utility’s state public utility commission, then must approve those rates. Regulators are required to allow utilities to recover all of their operating costs in their electricity rates. Consequently, they cannot simply bar utilities from including in their rates the costs associated with increased data center demand.

But regulators do have the ability to establish different rates for different classes of customers. And general regulatory principles provide that customers should be charged the costs incurred to provide their service. This means that regulators have the ability to establish a separate customer class for data centers. They can then allocate to this separate customer class all of the additional costs associated with data center demands for electricity. In this way, regulators can protect their other customers from having to pay higher electricity prices based on the costs caused by data center demand for electricity.

It would be relatively simple to determine the cost of upgrades incurred to deliver electricity to data centers served by a utility and to allocate all of those costs to the rates charged to those data centers. These costs are calculated before an upgrade is constructed and are easy to identify. But it is not necessarily an easy thing to identify and assign to data centers all of the other costs associated with their demand for electricity. For example, it would be much more difficult to determine how much of any particular RTO-wide capacity or energy market price is attributable to a data center or group of data centers. Nevertheless, regulators have the authority to set utility retail rates in such a manner as to protect utility retail customers, at least to some extent, from price increases caused by data centers’ increasing demand for electricity.

I have not done a survey of how state utility commissions have set the prices of the electricity their utilities charge to data centers, but I do not think that many states to date have attempted to allocate greater costs to data center rates to compensate for the increased costs data centers impose on utilities. To the contrary, I understand that, in some states, data centers have been offered relatively low electric rates as an incentive to locate data centers in that state. The states do, of course, have the prerogative to offer this type of incentive to data centers if they believe the benefits outweigh the costs. But doing so requires that other customers pay more for their electricity.

***

I hope you enjoyed this post. I enjoy writing them and will never charge for subscriptions or ask for donations. I only ask that, if you did enjoy it, you press the “like” button below. And please consider sharing my posts with other people you think might be interested. Doing so will help me evaluate interest in the book I am writing on grid operations. Of course, if you have a reaction to, or question about, this post, please leave a comment and I will be happy to respond.

[1] I know I wrote a post last November on whether data center demand causes electricity price increases (How Does the Explosive Growth of Ai’s Electric Demand Affect the Price of Electricity?), but I have some additional thoughts based on developments since then and more thinking about the issue.

[2] To translate a megawatt/day price into an annual charge for capacity, it is necessary to multiply the price by the 365 days of the year. For example, with the current $270 capacity price, the capacity price paid for each megawatt of a generation facility’s capacity would be 365 time $270 which equals $98,550. The capacity price paid for a not very large 100 megawatt facility would be $9,855,000, and for a large 1,000 megawatt facility $98,550.000.

[3] If you are interested, I provided a more detailed post about PJM’s recent capacity auctions in my January 18, 2026 post, PJM Failed to Acquire the Capacity it Needs to Ensure Reliability. What Does it Mean?

[4] I discussed this auction and its implications in more detail in my January 18, 2026 post, Pjm Failed to Acquire the Capacity it Needs to Ensure Reliability. What Does it Mean?

[5] THE STACK made its debut in Explaining the Grid Part Three—Market Products, and then made a repeat appearance in Explaining the Grid Part Four—RTO Energy Markets.

The LBNL/Brattle finding about the spread of utilization costs is the part most coverage misses — the beach house analogy lands.

Quick question on Part 2: PJM's last two auctions cleared at a FERC-approved cap of around $333/MW-day, and PJM estimated the uncapped price would have been closer to $530. When the cap expires, do you think state-level rate-class solutions like Virginia's are sufficient, or does the cost-allocation problem need to be solved at the RTO level?

Thank you for this article. I have two comments.

There is bad load growth and there is good load growth. Environmental advocates decry bad load growth associated with data centers because it affects affordability. They ignore the fact that their quest to decarbonize the economy will also increase load growth but that is all in a good cause.

Your description of THE STACK raises another unacknowledged environmental advocacy issue. The use of a magical cap-and-invest program that can ensure compliance while simultaneously raising money to pay for the transition assumes that the only costs are associated with the purchase of allowances. Those proceeds fund all sorts of favored efforts and the cost of transition if there is anything left over. What they do not realize is that cap-and-invest in the electric sector raises generator costs and affects THE STACK payouts so consumers are paying for that aspect too. I think this could easily double the cost for the Regional Greenhouse Gas Initiative program but all that money goes to the generators including those that have no compliance obligations.